29. Job Search II: Search and Separation#

Contents

29.1. Overview#

Previously we looked at the McCall job search model [McC70] as a way of understanding unemployment and worker decisions.

One unrealistic feature of the model is that every job is permanent.

In this lecture we extend the McCall model by introducing job separation.

Once separation enters the picture, the agent comes to view

the loss of a job as a capital loss, and

a spell of unemployment as an investment in searching for an acceptable job

using LinearAlgebra, Statistics

using Distributions, LaTeXStrings, NLsolve, Plots

29.2. The Model#

The model concerns the life of an infinitely lived worker and

the opportunities he or she (let’s say he to save one character) has to work at different wages

exogenous events that destroy his current job

his decision making process while unemployed

The worker can be in one of two states: employed or unemployed.

He wants to maximize

The only difference from the baseline model is that

we’ve added some flexibility over preferences by introducing a utility function

It satisfies

29.2.1. Timing and Decisions#

Here’s what happens at the start of a given period in our model with search and separation.

If currently employed, the worker consumes his wage

If currently unemployed, he

receives and consumes unemployment compensation

receives an offer to start work next period at a wage

He can either accept or reject the offer.

If he accepts the offer, he enters next period employed with wage

If he rejects the offer, he enters next period unemployed.

When employed, the agent faces a constant probability

(Note: we do not allow for job search while employed—this topic is taken up in a later lecture)

29.3. Solving the Model using Dynamic Programming#

Let

Here value means the value of the objective function (29.1) when the worker makes optimal decisions at all future points in time.

Suppose for now that the worker can calculate the function

Then

and

Let’s interpret these two equations in light of the fact that today’s tomorrow is tomorrow’s today.

The left hand sides of equations (29.2) and (29.3) are the values of a worker in a particular situation today.

The right hand sides of the equations are the discounted (by

But tomorrow the worker can be in only one of the situations whose values today are on the left sides of our two equations.

Equation (29.3) incorporates the fact that a currently unemployed worker will maximize his own welfare.

In particular, if his next period wage offer is

Equations (29.2) and (29.3) are the Bellman equations for this model.

Equations (29.2) and (29.3) provide enough information to solve out for both

Before discussing this, however, let’s make a small extension to the model.

29.3.1. Stochastic Offers#

Let’s suppose now that unemployed workers don’t always receive job offers.

Instead, let’s suppose that unemployed workers only receive an offer with probability

If our worker does receive an offer, the wage offer is drawn from

He either accepts or rejects the offer.

Otherwise the model is the same.

With some thought, you will be able to convince yourself that

and

29.3.2. Solving the Bellman Equations#

We’ll use the same iterative approach to solving the Bellman equations that we adopted in the first job search lecture.

Here this amounts to

make guesses for

plug these guesses into the right hand sides of (29.4) and (29.5)

update the left hand sides from this rule and then repeat

In other words, we are iterating using the rules

and

starting from some initial conditions

Formally, we can define a “Bellman operator” T which maps:

In which case we are searching for a fixed point

As before, the system always converges to the true solutions—in this case,

the

A proof can be obtained via the Banach contraction mapping theorem.

29.4. Implementation#

Let’s implement this iterative process

using Distributions, LinearAlgebra, NLsolve, Plots

function solve_mccall_model(mcm; U_iv = 1.0, V_iv = ones(length(mcm.w)),

tol = 1e-5,

iter = 2_000)

(; alpha, beta, sigma, c, gamma, w, dist, u, p) = mcm

# parameter validation

@assert c > 0.0

@assert minimum(w) > 0.0 # perhaps not strictly necessary, but useful here

# necessary objects

u_w = mcm.u.(w, sigma)

u_c = mcm.u(c, sigma)

# Bellman operator T. Fixed point is x* s.t. T(x*) = x*

function T(x)

V = x[1:(end - 1)]

U = x[end]

[u_w + beta * ((1 - alpha) * V .+ alpha * U);

u_c + beta * (1 - gamma) * U + beta * gamma * dot(max.(U, V), p)]

end

# value function iteration

x_iv = [V_iv; U_iv] # initial x val

xstar = fixedpoint(T, x_iv, iterations = iter, xtol = tol, m = 0).zero

V = xstar[1:(end - 1)]

U = xstar[end]

# compute the reservation wage

wbarindex = searchsortedfirst(V .- U, 0.0)

if wbarindex >= length(w) # if this is true, you never want to accept

w_bar = Inf

else

w_bar = w[wbarindex] # otherwise, return the number

end

# return a NamedTuple, so we can select values by name

return (; V, U, w_bar)

end

solve_mccall_model (generic function with 1 method)

The approach is to iterate until successive iterates are closer together than some small tolerance level.

We then return the current iterate as an approximate solution.

Let’s plot the approximate solutions

We’ll use the default parameterizations found in the code above.

function mcall_model(; alpha = 0.2,

beta = 0.98, # discount rate

gamma = 0.7,

c = 6.0, # unemployment compensation

sigma = 2.0,

u = (c, sigma) -> (c^(1 - sigma) - 1) / (1 - sigma),

w = range(10, 20, length = 60), # wage values

dist = BetaBinomial(59, 600, 400)) # distribution over wage values

p = pdf.(dist, support(dist))

return (; alpha, beta, gamma, c, sigma, u, w, dist, p)

end

mcall_model (generic function with 1 method)

# plots setting

mcm = mcall_model()

(; V, U) = solve_mccall_model(mcm)

U_vec = fill(U, length(mcm.w))

plot(mcm.w, [V U_vec], lw = 2, alpha = 0.7, label = [L"V" L"U"])

The value

At this point, it’s natural to ask how the model would respond if we perturbed the parameters.

These calculations, called comparative statics, are performed in the next section.

29.5. The Reservation Wage#

Once

If

If

Suppose in particular that

Then, since

We denote this wage

Optimal behavior for the worker is characterized by

if the wage offer

if the wage offer

If

Let’s use it to look at how the reservation wage varies with parameters.

In each instance below we’ll show you a figure and then ask you to reproduce it in the exercises.

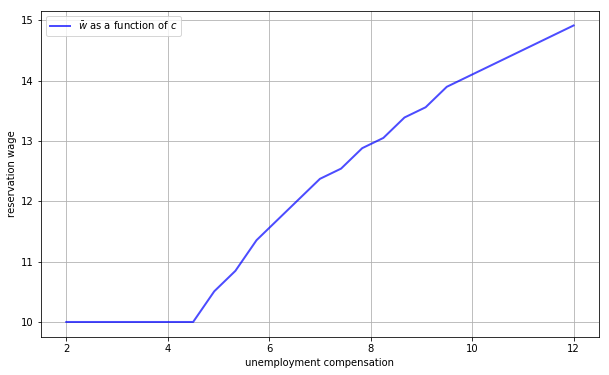

29.5.1. The Reservation Wage and Unemployment Compensation#

First, let’s look at how

In the figure below, we use the default parameters in the mcall_model tuple, apart from c (which takes the values given on the horizontal axis)

As expected, higher unemployment compensation causes the worker to hold out for higher wages.

In effect, the cost of continuing job search is reduced.

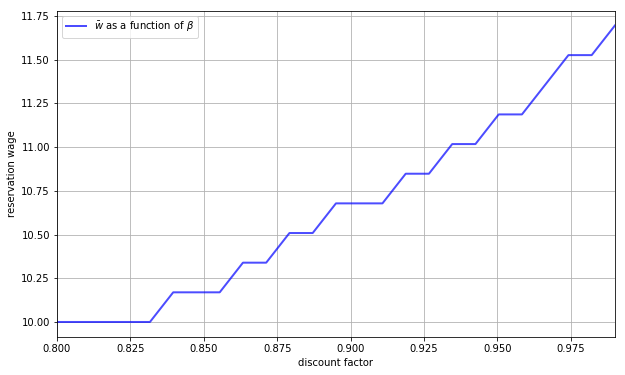

29.5.2. The Reservation Wage and Discounting#

Next let’s investigate how

The next figure plots the reservation wage associated with different values of

Again, the results are intuitive: More patient workers will hold out for higher wages.

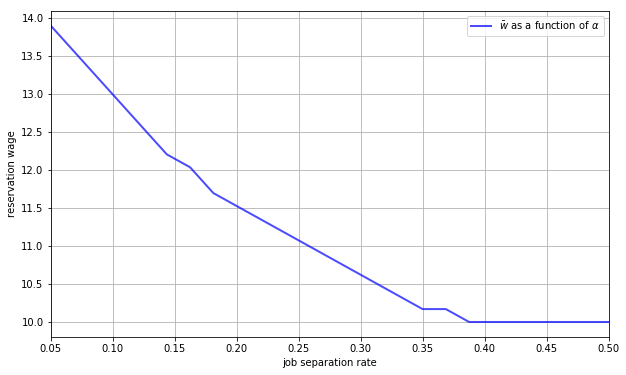

29.5.3. The Reservation Wage and Job Destruction#

Finally, let’s look at how

Higher

Once more, the results are in line with our intuition.

If the separation rate is high, then the benefit of holding out for a higher wage falls.

Hence the reservation wage is lower.

29.6. Exercises#

29.6.1. Exercise 1#

Reproduce all the reservation wage figures shown above.

29.6.2. Exercise 2#

Plot the reservation wage against the job offer rate

Use

gamma_vals = range(0.05, 0.95, length = 25)

0.05:0.0375:0.95

Interpret your results.

29.7. Solutions#

29.7.1. Exercise 1#

Using the solve_mccall_model function mentioned earlier in the lecture,

we can create an array for reservation wages for different values of

c_vals = range(2, 12, length = 25)

models = [mcall_model(c = cval) for cval in c_vals]

sols = solve_mccall_model.(models)

w_bar_vals = [sol.w_bar for sol in sols]

plot(c_vals,

w_bar_vals,

lw = 2,

alpha = 0.7,

xlabel = "unemployment compensation",

ylabel = "reservation wage",

label = L"$\overline{w}$ as a function of $c$")

Note that we could’ve done the above in one pass (which would be important if, for example, the parameter space was quite large).

w_bar_vals = [solve_mccall_model(mcall_model(c = cval)).w_bar

for cval in c_vals];

# doesn't allocate new arrays for models and solutions

29.7.2. Exercise 2#

Similar to above, we can plot

gamma_vals = range(0.05, 0.95, length = 25)

models = [mcall_model(gamma = gammaval) for gammaval in gamma_vals]

sols = solve_mccall_model.(models)

w_bar_vals = [sol.w_bar for sol in sols]

plot(gamma_vals, w_bar_vals, lw = 2, alpha = 0.7, xlabel = "job offer rate",

ylabel = "reservation wage",

label = L"$\overline{w}$ as a function of $\gamma$")

As expected, the reservation wage increases in

This is because higher

Hence workers are less willing to accept lower offers.